Assessing finance charges is a complicated process. But if you have a lot of late payments coming in, you may want to consider it.

There are many reasons why your customers send in payments past their due dates. Maybe they missed or misplaced your invoice, or they’re disputing the charges. They might not be very conscientious about bill-paying. Or they simply don’t have the money.

Sometimes they contact you about their oversight, but more often, you just see the overdue days pile up in your reports.

You could use stronger language in your customer messages. Send statements. Make phone calls if the delinquency goes on too long. Or you could start assessing finance charges to invoices that go unpaid past the due date. QuickBooks provides tools to accommodate this, but you’ll want to make absolutely sure you’re using them correctly – or you’ll risk angering customers and creating problems with your accounts receivable.

Setting the Rules

Before you can start, you’ll need to tell QuickBooks how you’d like your finance charges to work. It’s at this stage that we recommend you let us work with you. There’s nothing overly difficult about understanding finance charges in theory: you apply a percentage of the dollar amount that’s overdue to come up with a new total balance. But setting up your QuickBooks file with the finance charge rules you want to incorporate may require some assistance. If it’s done incorrectly, you will hear from your customers.

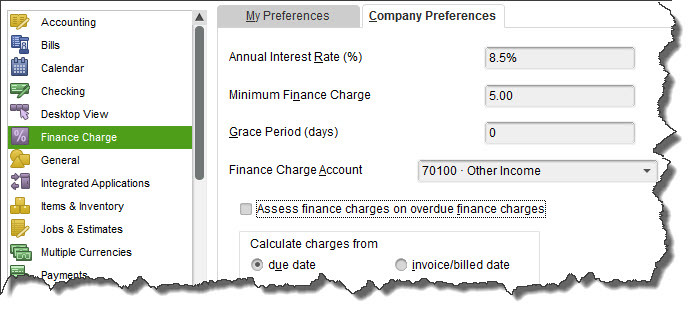

Here’s how it works. Open the Edit menu and select Preferences, then Finance Charge | Company Preferences.

Figure 1: Before you can start adding finance charges to overdue invoices, you’ll need to establish your company preferences.

Figure 1: Before you can start adding finance charges to overdue invoices, you’ll need to establish your company preferences.

What Annual Interest Rate percentage do you want to tack onto late payments? This is an issue we can discuss with you. Too low, and it’s not worth your extra time and trouble. To, high, and your customers may stop patronizing your business. And do you want to set a Minimum Finance Charge? Will you allow a Grace Period? If so, how many days?

You’ll need to assign an account to the funds that come in from interest charges. This needs to be an income account. In our example, it’s Other Income.

The next decision, whether to Assess finance charges on overdue finance charges, needs consideration – and some research. This may not be an option depending on the lending laws in the jurisdiction where your business is located. So again, if you want to charge interest on unpaid and tardy finance charges themselves, let’s talk.

When do you want the finance charge “countdown” to begin? When QuickBooks identifies a transaction that has not been paid within the stated terms, do you want the added charge to be applied based on the due date or the invoice/billed date?

Note: If your business sends statements rather than invoices, leave the Mark finance charge invoices “To be printed” box at the bottom of this window unchecked.

Applying the Rules

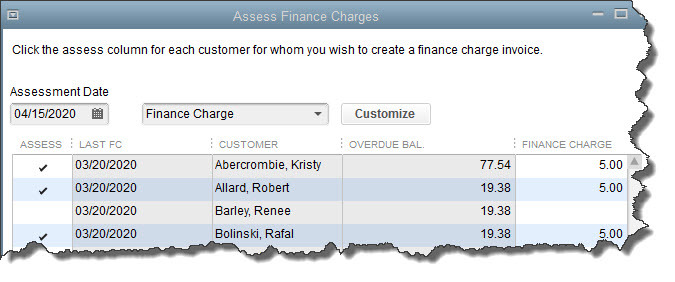

QuickBooks does not automatically add finance charges to your customers’ invoices. You’ll need to administer these additions yourself, though QuickBooks will handle the actual calculations. Open the Customers menu and select Assess Finance Charges to open this window:

Figure 2: You’ll determine who should have finance charge invoices created in the Assess Finance Charges window.

Figure 2: You’ll determine who should have finance charge invoices created in the Assess Finance Charges window.

Make very sure that the Assessment Date is correct, as it has impact on QuickBooks’ calculations. Being even a day off makes a difference. Select the customers who should have finance charges applied by clicking next to their names in the Assess column. QuickBooks will display the Overdue Balance from the original invoice, as well as the Finance Charge it has calculated.

- If you choose not to apply finances charges to a customer because he or she has provided a good reason for the late payment, be sure the box in the Assess column is unchecked.

- If you want to change the finance charge due for a valid reason, you can type over the amount in the last column. This would be a rare occurrence and should be exercised only after consulting with us.

Important: If there is an asterisk next to a customer’s name, there are payments or credit memos that have not yet been applied to any invoice.

When everything is correct, click the Assess Charges button at the bottom. QuickBooks will create separate invoices for finance charges for each customer who owes them.

We can’t stress enough the importance of consulting with us before you start to work with finance charges enough. Keep your company file accurate and your customers happy by getting this complex accounting element right from the start.